Testamentary Trusts

Trusts with the ease of a last will and testament

Maryland Testamentary Trust Lawyer

Many clients would like to have some benefits of a trust but also want the simplicity of setting up a last will and testament. Using a testamentary trust, your Maryland trusts and estate attorney may be able to provide you exactly that.

An important tool for sustaining your family

While living trusts get far more attention, Maryland estate attorneys create testamentary trusts far more often than all others.

What is a testamentary trust?

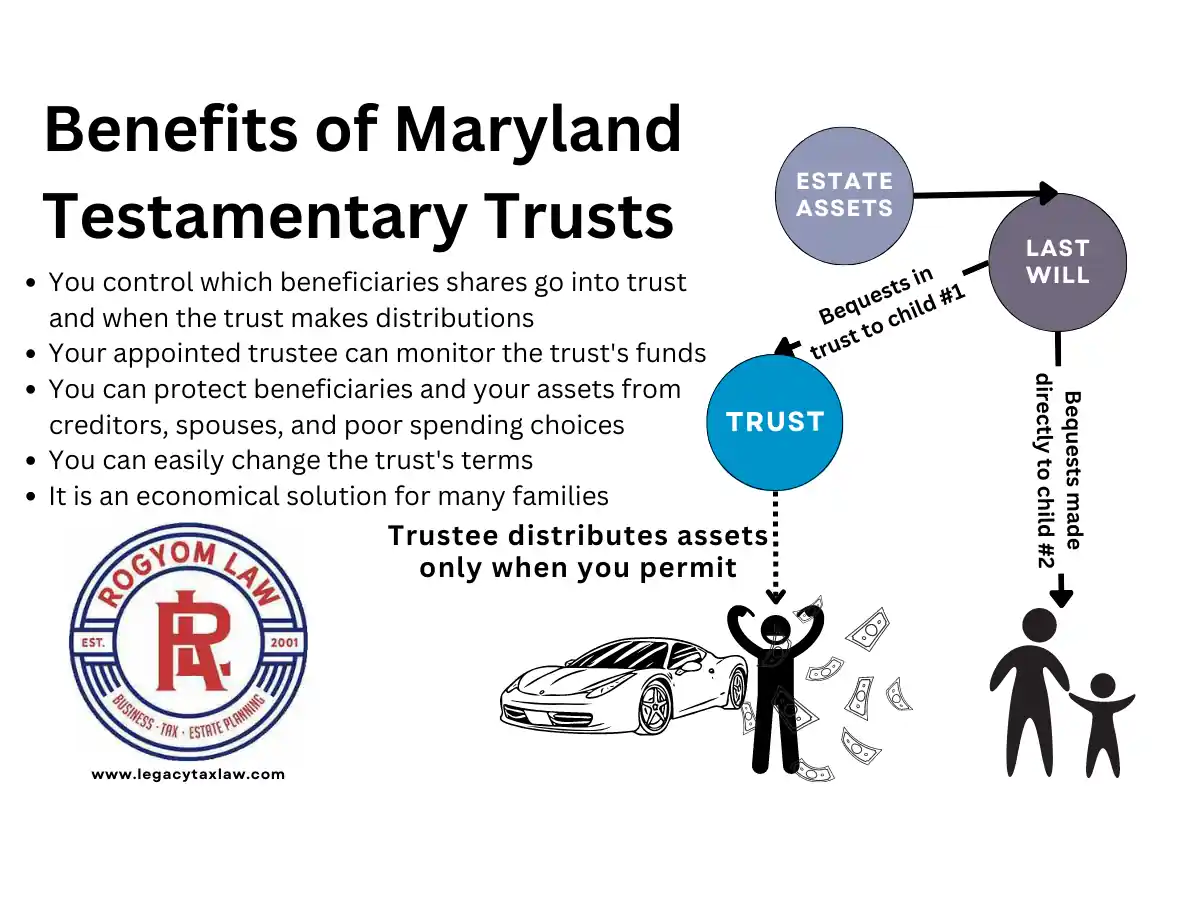

A testamentary trust is a legal trust created in your will to provide support for a beneficiary when you die. It allows you to provide for your spouse, children, and other beneficiaries without immediately giving them unrestricted access and control of the inherited assets.

Similar to other Maryland trusts, parties to a testamentary trust include:

- Settlor – the person who creates the trust, in this case the person who created the will;

- Trustee – the person who will control the trust and its assets; and

- Beneficiary – the one or more people receiving the benefits of the trust.

The trust will own any property transferred to it, rather than any individual.

The purpose of a testamentary trust

A Maryland estate planning attorney will use testamentary trusts for many client purposes. The most common would be if you want to leave your estate to your spouse, children, or grandchildren, but you know it’s not in their best interests to receive it all immediately upon your death.

Because of the ability to distribute the assets over time, Maryland estate lawyers often use a last will with a testamentary trust to:

- Provide for a surviving spouse

- Allow children and grandchildren to receive assets while supervised

- Provide for spouses, children, and step-children in blended families

The trustee will be required to distribute the assets to the beneficiaries according to the instructions that you, the creator of the trust, provide in your last will and testament. The last will and testament will include all terms of the trust, including naming the trustee, instructions on how to invest the assets, and the rules for making distributions from the trust.

How does a testamentary trust work?

A last will and testament with a testamentary trust contains the typical language of a last will and testament. As usual, the last will and testament names the estate’s personal representative, names your estate’s beneficiaries, and describes how to divide the property.

The testamentary trust will then have one or more clauses that will state that the assets given to a beneficiary will fund a trust.

For example, if there is a trust established for children or grandchildren, the last will and testament may have a clause stating that if a beneficiary is under the age of 35, then their share of the estate will transfer to the trust.

The last will and testament then provides the terms of the trust. The last will and testament must include all provisions normally found in a trust agreement.

When the Trustee should distribute assets to the beneficiary will be a part of the trust’s terms. It will also state who will be the trustee, how the trustee can invest the trust’s funds, what to do with the trust’s funds if the beneficiary passes away, and other terms on how to administer the trust.

When the person passes away, your family and the Maryland probate attorney will open the estate like usual with the Maryland register of wills for that county. Rather than distributing the share to that beneficiary, the estate will use that beneficiary’s share to fund that person’s trust. The trust will continue to hold the assets according to the trust’s terms.

Ready to get started? We’re Ready to Help.

Contact us now and we’ll be happy to schedule a call or meeting with no commitment.

If we cannot assist you, we will gladly provide you with referrals.

Pros of a Testamentary Trust in Maryland

Many advantages of a testamentary trust in Maryland make them very popular with clients and Maryland estate planning attorneys. Some of those positives include:

Cost Savings

You can usually expect to pay less for a testamentary trust than for a living trust. This is for several reasons. The attorney includes the testamentary trust in the client’s last will and testament, so there is one less document to create. Further, living trusts require you to fund them to be effective.

In other words, if you want the living trust to include your real estate, then you will need to transfer the title to the property from you to the trust. In contrast, you do not need to fund a testamentary trust during your lifetime. It simply takes assets from your estate upon your death and puts them into the trust.

Easier to Set Up

You do not need to fund a testamentary trust during your lifetime. You avoid the sometimes costly and time-consuming process of funding the trust. Your estate will transfer assets to your testamentary trust, rather than directly to the trust’s beneficiaries.

For example, if you want your home to go into the trust for your children, a living trust requires you to transfer the title of the property to the trust. If it were a testamentary trust, your estate’s personal representative would transfer the property to the trust following your death.

Ability to Change

You can easily change a testamentary trust and the assets going to it. You can alter the trust’s terms, beneficiaries, and assets until death.

Since you may fund a living trust prior to death, if you want to change the assets going to it, you may need to transfer those assets either back to you or to another trust.

Being able to change a living trust will depend upon whether you make it revocable or irrevocable. A living trust’s status as revocable or irrevocable determines whether you can change it.

Protecting Assets of Beneficiaries

You can use a testamentary trust to protect assets going to your beneficiaries. Since you can delay the trust distributing assets to your beneficiaries using a testamentary trust and can set the terms of the trust agreement, you can shield the assets you put into the trust from creditors and any other type of person who may want to get their hands on what you leave to the beneficiary.

Disadvantages of Testamentary Trusts

Probate May Be Needed

If using a testamentary trust, your family will need to go through the probate process to have your estate’s assets transferred from you to the trust. If you had used a living trust, the assets of the trust would already be in the trust prior to your death. A living trust would simply convert to being an irrevocable trust and the trustee would begin distributing trust assets to your beneficiaries instead.

Privacy Issues

Anyone can see the terms of the testamentary trust, because your family will file the last will and testament with the Maryland Register of Wills for your county. They will also be able to see any probate assets going into the trust. For some families, this may be more of a concern, particularly if the testamentary trust will include terms addressing drug, health, or other personal matters.

Trust Terms

Depending upon your arrangements for storing and filing your last will and testament, your family may see the terms of your last will and testament and its trust prior to filing. Unfortunately, it’s not uncommon for a last will and testament to be misplaced, whether or not by accident, and not filed.

In contrast, your family will often be able to find a trust agreement for a living trust with any banks, financial advisor, and others holding the trust’s assets. Those companies often require a copy of the trust agreement when you fund it, and they will not allow access to the funds unless the trust agreement allows.

Creditors of the Estate

Creditors will have a much simpler task of determining their ability to collect and the ability to file a claim against the estate, since the assets used to fund the testamentary trust will become publicly knowledge.

In contrast, while the assets in a living trust may be subject to judgements and other creditor actions, a creditor would need to use a lot more effort to identify the assets and collect on their claim.

The living trust holds assets in the trust’s name, making discovering them more difficult. Creditors of an estate, however, can file simple creditor claim and the personal representative will be required to pay all legitimate claims before making any distributions from the estate.

Ability to Change

Your ability to a trust s a positive aspect of a testamentary trust, but it can also be a negative.

Since we live longer today, many more people will become dependent upon others. Unfortunately, we become more susceptible to being taken advantage of. Because of that dependence, greedy caregivers or family members can sometimes coerce the elderly to sign documents to change their estate plan.

If a person coerced you into changing your last will and testament, then they would eliminate the testamentary trust together with the assets. On the other hand, your funding the living trust eliminates those assets from your estate.

Further, few would know the process of changing a living trust without consultation with your attorney and others. If they changed the last will and testament, it would not affect those assets already transferred to a living trust and could stop their plan to steal from your family.

Types of Testamentary Trusts

While we can use testamentary trusts for many purposes, these are the most common uses:

Children and Grandchildren Trusts

Maryland estate lawyers usually recommend using trusts if some heirs are under a certain age. The most common ages seem to be 30, 35, or 40. Families usually choose an age where they feel the child or young adult will be past an age where most make their mistakes, whether it’s spending, poor investments, bad marriages, or similar.

Your Maryland estate attorney will draft the last will and testament so the portion of your estate that will go to the child or grandchild will go into a trust if the child is under the designated age. The trust allows the trustee to distribute assets to the child or their benefit for their Health, Education, Maintenance, and Support (HEMS) of the child.

You also can determine what additional expenses the trust can pay. You can also add or restrict the allowed expenses away from HEMS. So, you can state you want the trust to contribute to their wedding or not pay for graduate school.

At a certain point, the children’s trust distributes assets to the child until distributing all trust assets. Most choose to have the trust distribute the assets in two or three portions. For instance, you may choose to have the trust make the distributions at ages 25, 30, and 35.

We can include special provisions in the trust to delay distributions as long as necessary if the child has addiction or similar issues.

Spousal Trusts

While many spouses will elect to title assets so the spouse will become the owners of their property following their death, some prefer those spouses receive the use or income of the property and then have the remaining assets go to their children. Blended families, those with children from previous marriages, find particular uses of spousal trusts, since it protects the assets in the trust and then gives those assets to their respective children.

Bypass Trusts

Bypass trusts have become less common since the increased estate tax deduction eliminates estate tax concerns for all but the most wealthy. Nonetheless, there are still instances where these may be needed. The bypass trust is a special form of spousal trust. A bypass trust uses the estate tax deduction of each spouse.

The attorney will create two trusts, each using the estate tax deduction of each spouse. The assets going into one trust uses the estate tax deduction of the first spouse to die and the second trust uses the estate tax deduction of the surviving spouse to pass the remaining assets to your family.

Special Needs Trusts

Families that have members with disabilities may use testamentary trusts with provisions that will eliminate those assets to calculate the assets of the person with disabilities. The trust works similar to a children’s trust, but Social Security, Medicaid and other government agencies will not count the trusts’ assets since the beneficiary will have limited rights to trust distributions.

A provision will typically state the trustee has complete discretion over distributions and freezes distributions that would cause a reduction in the disabled person’s Social Security, Medicaid, or similar benefits.

Trusts of Business Purposes

You may have interests in a business or real estate that your family may be unable to manage wisely if you were not available. While a business or property manager may be employed by the family after your death, often the family may not be able to fill the role of the business’s owner. Having a testamentary trust and its trustee fill that role can be key to your business surviving and your real estate empire continuing to thrive.

Which is better for you, a Maryland living trust or a testamentary trust?

Testamentary trusts and living trusts provide some of the same benefits. The differences between Maryland living trusts and testamentary trust may make one a better choice for you and your family.

Age as a factor for testamentary trusts

The Maryland estate attorney will consider your age when deciding whether we use a living trust or a testamentary trust in your particular case. While your age may not affect your need for estate planning, it can affect the methods used for planning.

A testamentary trust gives you more flexibility for future planning. If you don’t like your current plan, then you can change the last will and testament that creates it. If using a living trust, you will need to keep assets titled in the living trust’s for the remainder of your life and changing the trust and its assets gets more complicated. As we age, living trusts can become a more sensible choice.

Health factors for testamentary trusts

If family history or personal health make you believe you could soon become incapable of making choices or become susceptible to some less than scrupulous relatives or caregivers, then a living trust will be far more difficult for them to force you to change.

While it’s easy to draw up a quick last will and testament, that same person may not be aware the trust exists, know how to change it, or realize the trust owns the most valuable assets.

Thus, if they coerce you into signing a new last will, your trust and the assets titled to it will be unaffected.

Costs of forming trusts

You can usually expect to pay higher set up fees for forming a living trust than to have a testamentary trust. The cost difference can be substantial since living trusts also require you to retitle assets to it. This can obviously be a factor to be considered.

Tax basis of assets when forming trusts

All assets included in your last will and testament and passed through your estate will receive a step-up in basis if they have appreciated by the time of your death. This will eliminate any gain and recapture of depreciation if your heirs sell those assets.

If the assets funding the testamentary trust pass through your estate as usual, then they will also receive a stepped-up basis. While most revocable living trusts also receive this benefit, this is not always the case.

Other considerations

While the above are some of the more common considerations, your Maryland trust attorney may discover some factors during your consultation that will affect which type of trust to use.

Conclusion

A testamentary trust has many benefits and your Maryland estate and trust attorney may suggest using one as part of your estate plan. Your family’s specific circumstances and goals will determine whether you should use a testamentary trust as part of your estate plan.

Common Questions about Maryland Testamentary Trusts:

When does a testamentary trust take effect?

A testamentary trust does not take effect until the death of the person who created the trust in their last will and testament.

The person creating the testamentary trust does not need to maintain the trust during their lifetime. Maryland and the IRS will not require the trust to file tax returns. But this also means you cannot put assets into its name until death as well.

So, for instance, if you owned a home in Timonium and want to transfer the property to the trust during your lifetime, this is not possible with a testamentary trust. The home will need to included as part of your estate with the Register of Wills for Baltimore County. Once probate is completed, the estate will transfer the home to the trust.

What types of property can go into a testamentary trust?

You can put any type of property you may own into a testamentary trust. In fact, you may decide you want to have more than one testamentary trust in your last will and testament to deal with different property types.

For instance, let’s say you live near Jacksonville, Maryland and still own your family farm near Boonsboro. You have investments and other assets you assume the estate will sell after your death. If you would like to keep the Washington County farm in the family, you may decide to include a trust specifically for to keep that property intact and maintained for the long-run.

How long can a testamentary trust last?

You have the option of how long the trust will last. Some people want the trust to last for a very short time period while others will only want the minimal amounts distributed each year and continue on for multiple generations. The choice is yours.

Who should be the trustee of a testamentary trust?

You will obviously want someone you can trust to be the trustee. It’s often important to have someone with some connection to the beneficiary. For instance, if you form a trust to benefit a grandchild, you may want that grandchild parent or sibling to be its trustee, since they will be familiar with their person and their needs.

Can I change my testamentary trust?

So long as you can change your last will and testament, you can change the terms of a testamentary trust. You can also change what assets will go into the trust or eliminate the trust altogether by changing your last will and testament.

What happens if the beneficiary of a testamentary trust if they pass away?

If the beneficiary passes away before you, then the assets will go to the others you name in your last will and testament. You may have provided that the beneficiary’s share will go to their children if there are any and, if not, then to their siblings. The will may state that the share of that child will go into the trust.

If the beneficiary passes away after you have died, then the trust often provides what will happen with those assets. Often, it will state that the remaining assets will go to the children of the beneficiary if any are living.

Can I contribute to a testamentary trust?

Prior to the death of the person who created the testamentary trust, its grantor, you could not transfer assets to that trust. The settlor’s death marks the formation of the trust and the first time at which you or its settlor can make contributions to it.

After the testamentary trust’s formation, the last will and testament will transfer assets to the testamentary trust and any non-probate assets, life insurance, investments, and similar, that designate the trust as its beneficiary.

If you did not form the testamentary trust but wish to contribute to it, then it may be possible. The trust agreement dictates whether others may make contributions to the trust. The trustee may have the discretion on whether to allow contributions if the trust agreement is silent on the topic.

TESTIMONIALS